- News

- Horse Racing

- Racing Preview

- AQHA Racing Challenge

- Breeding

- Sales

- Quick Stakes Results

- Detail Race Results

- Qualifiers

- Leader Board

- Leading Sires

- Videos

- Auction Leaders

- Q-Racing

Streaming Video

Photo by:

Kristina Bowman

by Tad Davis

WASHINGTON, DCSEPTEMBER 14, 2009Thanks to the 2009 Economic Stimulus Bill and the new depreciation schedule for race horses that became effective this year, 2009 is a great year to buy a racing Quarter Horse.

The depreciation and expensing allowances have never been better. Buyers may be able to write off a substantial portion of the cost of the horse in the year of purchase--if not the entire cost of the purchase.

The more generous write-off allowances for Quarter Horses and other race horses purchased this year result from three changes to the tax law, all of which come into play in 2009. The Economic Stimulus Bill continued bonus depreciation for 2009, which allows a deduction of 50 percent of the cost of a yearling. In addition, it continued the higher expense deduction into 2009, which allows a taxpayer to deduct up to $250,000 of the cost of a horse in the year it is purchased. As is usually the case in the tax law, there are some limitations and requirements that apply to both provisions.

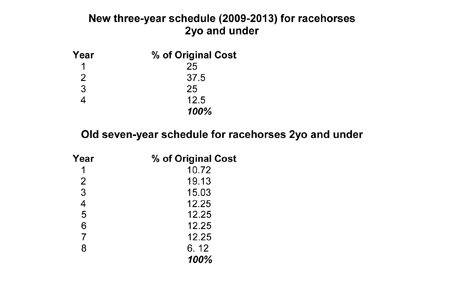

The third change, contained in the Farm Bill, allows all racehorses to be depreciated over three years (four tax years). Prior to 2009, yearlings had to be depreciated over seven years (eight tax years). As the table below shows, the first year deduction is 2.5 times better than in prior years and could be three times better if the purchaser is only engaged in racing, and not racing and breeding, or just breeding. (A wrinkle in the tax law that is best explained by one's tax advisor.) The new rules let the purchaser write off 62.5% of the cost in the first two years or almost 75% of the cost if the purchaser is engaged only in racing.

Applying all of these write-off benefits to the purchase of a yearling this year can produce rather dramatic results. For example, if a buyer purchases a Quarter Horse yearling this year for $150,000 and buys no other horses or depreciable business property during the year, he can expense (i.e., write off) the entire cost.

Even If he buys two more yearlings for $75,000 each, he can still write off the entire $150,000 cost of the first yearling he bought and he can expense $100,000 of the cost of the other two yearlings, each purchased for $75,000 (allocated any way he chooses). Thus, he could have a total expense deduction of $250,000. In addition, he would be able to take a depreciation deduction of $12,500 on the $50,000 balance of the cost of the purchase of the two yearlings, for a total write-off of $262,500 in 2009. That works out to be 87.5% of the total $300,000 cost of the three yearlings. If the buyer is only engaged in racing, and not in both racing and breeding, he can use a slightly better depreciation rate that would result in $4,150 more depreciation in 2009.

The expense deduction is reduced dollar-for-dollar as purchases of horses and any other depreciable property used in your business exceed $800,000 during the year. Thus, the expense deduction is zero once purchases during the year hit $1,050,000.

In the above example, had the buyer purchased $1,250,000 of horses, including the yearlings, in 2009, he would not be entitled to the $250,000 expense allowance since total purchases would have exceeded $1,050,000. He could still take bonus depreciation on the total cost of the yearlings (50% X $300,000 = $150,000) and regular depreciation on the balance using the new rules (25% X the balance of $150,000 = $37,500). The total depreciation deduction would be $187,500 in 2009, or 62.5% of the cost of the yearlings. If the buyer is only engaged in the racing business, the total depreciation deduction could be about $12,500 more, bringing the deduction to about $200,000, almost 67% of the cost.

It is easy to see from the examples why the current tax benefits are good for the upcoming yearling sales this year. Next year's tax benefits will not be as good unless Congress extends the current package. Bonus depreciation expires at the end of this year and the $250,000 expense allowance goes down to $125,000 next year, with the dollar-for-dollar phase out starting at $500,000, instead of $800,000.

Assuming the economy continues to improve, it will probably be a long time before a buyer gets the generous first-year write-offs that are available for purchases this year. Tax incentives such as these aren't likely to last as the country recovers from recession and buyers should plan--and act--accordingly.

Thomas A. "Tad" Davis, Esq., is a partner in the law firm of Davis & Harman LLP. He specializes in legislative and administrative law issues, particularly in the areas of tax, financial markets and agricultural policy.

He is the author of Horse Owners and Breeders Tax Handbook, which is recognized as the leading authority on tax issues related to the equine industry.

©Copyright. This article may not be reproduced in any form or by any means, electronic or mechanical, without prior written permission of the copyright owner, Tad Davis.

|

||

Newsletters

Newsletters Facebook

FacebookCopyright © 2026 StallioneSearch, LLC, All rights reserved internationally.